Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Video •

February 5, 2025

VIDEO: 2025 Housing Market Forecasts (50 sec.)

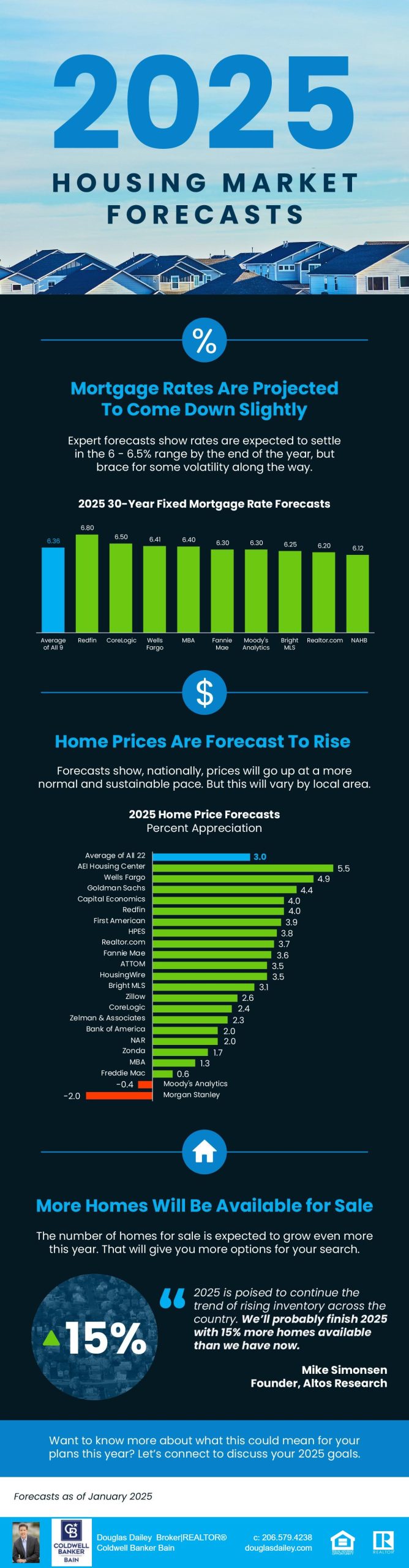

2025 Housing Market Forecasts

The latest 2025 forecasts show mortgage rates are projected to come down slightly, prices are forecast to rise, and more homes will be available for sale. Want to know more about what this could mean for your plans this year? Let’s connect.

Home Seekers •

February 5, 2025

BLOG: One Homebuying Step You Don’t Want to Skip

One Homebuying Step You Don’t Want To Skip: Pre-Approval

There’s one essential step in the homebuying process you may not know a whole lot about and that’s pre-approval. Here’s a rundown of what it is and why it’s so important right now.

What Is Pre-Approval?

Pre-approval is like getting a green light from a lender. It lets you know how much they’re willing to let you borrow for a home. To determine that number, a lender looks at your financial history. According to Realtor.com, these are some of the documents a lender may ask you for during this process:

- W-2s from the last two years

- Tax returns from the last two years

- Pay stubs from the last 30 days

- Bank statements from the last 60 days

- Investment account statements (if applicable)

- Two years of history of where you’ve lived

The result? You’ll get a pre-approval letter showing what you can borrow. Keep in mind, that any changes in your finances can affect your pre-approval status. So, after you receive your letter, avoid switching jobs, applying for new credit cards or other loans, or taking out large sums of money from your savings.

How It Helps You Determine Your Borrowing Power

This year, home prices are expected to rise in most places and mortgage rates are still showing some volatility. So, since affordability is still tight, it’s a good idea to talk to a lender about your home loan options and how today’s changing mortgage rates will impact your future monthly payment.

The pre-approval process is the perfect time for that. Because it determines the maximum amount you can borrow, pre-approval also helps you figure out your budget. You should use this information to tailor your home search to what you’re actually comfortable with as far as a monthly mortgage payment. That way, you don’t fall in love with a house that’s out of your comfort zone.

How It Helps You Stand Out

Once you find a home you want to put an offer on, pre-approval has another big perk. It not only makes your offer stronger, it shows sellers you’ve already undergone a credit and financial check.

When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Bottom Line

If you’re planning on buying a home, getting pre-approved for a mortgage should be one of the first things on your to-do list. Not only will it give you a better understanding of your borrowing power, it can put you in the best position possible to make a strong offer when you find a home you love. Connect with a trusted lender to learn more.

Home Sellers •

February 5, 2025

BLOG: Roughly 11,000 Homes Will Sell Today

Roughly 11,000 Homes Will Sell Today – Will Yours Be One of Them?

Are you hesitant to sell your house because you’re worried no one’s buying with rates and prices where they are right now? Here’s some perspective that can help.

The market actually isn’t at a standstill. While there weren’t as many sales last year as there’d be in a normal market, roughly 4.15 million homes still sold (not including new construction), according to the National Association of Realtors (NAR). And the expectation is that number will rise in 2025. That means more people will likely move this year, and they need homes to buy. Homes like yours.

But even if we only match last year’s sales pace, here’s what that looks like.

Every Minute Homes Are Selling – Literally

- 4.15 million homes ÷ 365 days in a year = 11,370 homes sell each day

- 11,370 homes ÷ 24 hours in a day = 474 homes sell per hour

- 474 homes ÷ 60 minutes = roughly 8 homes sell every minute

Think about that. Just in the time it took you to read this, 8 homes sold.

If you’ve been holding off on selling your house because you think buyers aren’t out there, let this reassure you – there are still buyers looking to buy.

Every day, thousands of people need to buy homes. So, while higher home prices and mortgage rates have slowed the market down and forced some buyers onto the sidelines, that doesn’t mean the market isn’t active. Many buyers are still eager to make a move because life doesn’t wait for perfect market conditions.

With the right agent by your side, you can get your house in front of those buyers while other hesitant homeowners are still putting their plans on pause because they’re worried buyer demand has disappeared. Let’s get your house sold.

Bottom Line

On average, over 11,000 homes sell every day, and yours could be one of them. In the time it took you to read this, another 8 homes sold.

When you’re ready to take the next step, let’s connect so you have an agent to create that perfect strategy.

Home Seekers •

February 5, 2025

BLOG: The Truth About Credit Scores

The Truth About Credit Scores and Buying a Home

Your credit score plays a big role in the homebuying process. It’s one of the key factors lenders look at to determine which loan options you qualify for and what your terms might be. But there’s a myth about credit scores that may be holding some buyers back.

The Myth: You Need To Have Perfect Credit

According to Fannie Mae, only 32% of potential homebuyers have a good idea of what credit score lenders actually require.

That means two-thirds of buyers don’t actually know what lenders are looking for – and most overestimate the minimum credit score needed.

The Reality: Perfect Isn’t Necessary

But the truth is, you don’t need perfect credit to become a homeowner. To see the average score, by loan type, for recent homebuyers check out the graph below:

There is no set cut-off score across the board. As FICO explains:

There is no set cut-off score across the board. As FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

So, even if your credit score isn’t as high as you’d like, you may still be able to get a home loan. Just know that, even though you don’t need perfect credit to buy a home, your score can have an impact on your loan options and the terms you’re able to get.

Work with a trusted lender who can walk you through what you’d qualify for.

Simple Tips To Improve Your Credit Score

If you want to open up your options a bit more after talking to a lender, here are a few tips from Experian and Freddie Mac that can help give your score a boost:

1. Pay Your Bills on Time

This includes everything from credit cards to utilities and other monthly payments. A track record of on-time payments shows lenders you’re responsible and reliable.

2. Pay Down Outstanding Debt

Reducing your overall debt not only improves your credit utilization ratio (how much credit you’re using compared to your total limit) but also makes you a lower-risk borrower in the eyes of lenders. That makes them more likely to approve a loan with better terms.

3. Hold Off on Applying for New Credit

While opening new credit accounts might seem like a quick way to boost your score, too many applications in a short period can have the opposite effect. Focus on improving your existing accounts instead.

Bottom Line

Your credit score doesn’t have to be perfect to qualify for a home loan. The best way to know where you stand? Work with a trusted lender to explore your options.

RE News •

January 31, 2025

BLOG: How Much Equity Have You Gained?

How Much Home Equity Have You Gained? The Answer Might Surprise You

Have you ever stopped to think about how much wealth you’ve built up just from being a homeowner? As home values rise, so does your net worth. And, if you’ve been in your house for a few years (or longer), there’s a good chance you’re sitting on a pile of equity — maybe even more than you realize.

What Is Home Equity?

Home equity is the difference between what your house is worth and what you owe on your mortgage. For example, if your house is worth $500,000 and you still owe $200,000 on your home loan, you have $300,000 in equity. It’s essentially the wealth you’ve built through homeownership. Right now, homeowners across the country are seeing record amounts of equity.

According to Intercontinental Exchange (ICE), the average homeowner with a mortgage has $319,000 in home equity.

Why Have Homeowners Gained So Much Equity?

The rise in home equity over the years can be credited to two key factors:

1. Significant Home Price Growth

Home prices have climbed dramatically in recent years. In fact, according to the Federal Housing Finance Agency (FHFA), over the past five years, home prices nationwide have risen by 57.4% (see map below):

This appreciation means your house is likely worth much more now than when you first bought it.

This appreciation means your house is likely worth much more now than when you first bought it.

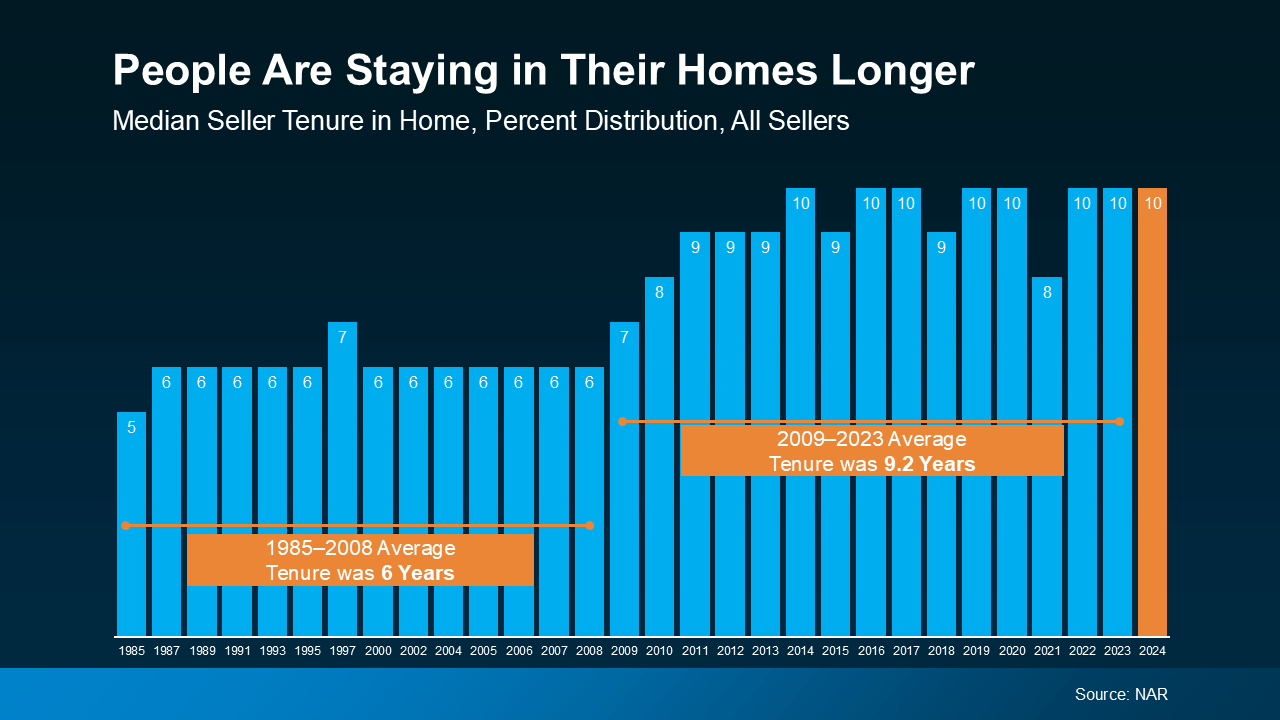

2. Longer Tenure in Homes

Data from the National Association of Realtors (NAR) shows people are staying in their homes for a decade (see graph below):

This increased tenure means homeowners benefit even more from home values growing over time. That’s because the longer someone has lived in their house, the more that home’s value has grown, which directly increases equity.

This increased tenure means homeowners benefit even more from home values growing over time. That’s because the longer someone has lived in their house, the more that home’s value has grown, which directly increases equity.

And if you’re one of those people who’s been in their home for 10 years or more, know this – according to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

The Benefits of Having Home Equity

What does that mean for you? It means your house might be your biggest financial asset — and it could open up some exciting opportunities for your future. Let’s break it down.

- Moving to Your Next Home

Your equity could help you cover the down payment for your next home. In some cases, it might even mean you can buy your next house all cash.

- Financing Home Improvements

Thinking about upgrading your kitchen, adding a home office, or tackling other projects? Your equity can provide the funds to make those improvements happen, increasing your home’s value and making it more enjoyable to live in too.

- Getting a Business Going

If you’ve been dreaming about starting your own business, your equity could be the kickstart you need. Whether it’s for startup costs, equipment, or marketing, leveraging your home’s value can help bring your entrepreneurial goals to life.

Bottom Line

Whether you’re thinking about selling, upgrading, or simply want to understand your options, your home equity is a powerful resource. If you’re wondering how much equity you’ve built or how you can use it to meet your goals, let’s connect and explore the possibilities.

Video •

January 31, 2025

VIDEO: How Mortgage Rates Accept Your Monthly Payments (53 sec.)

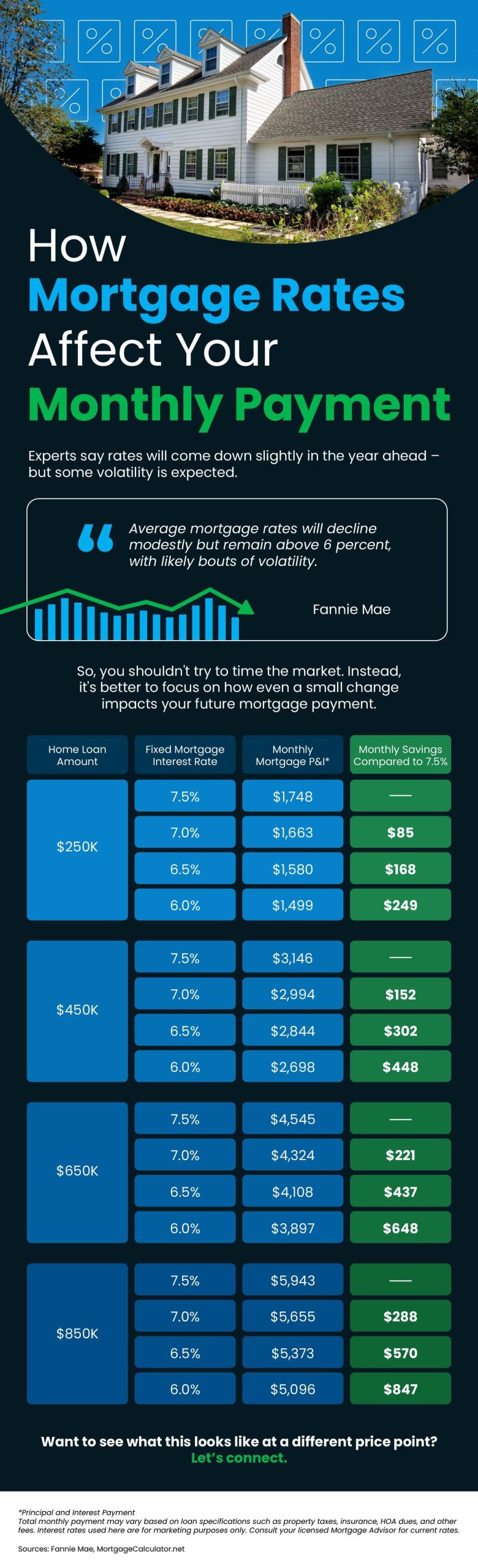

How Mortgage Rates Affect Your Monthly Payment

Experts say rates will come down slightly in the year ahead – but some volatility is expected. So, you shouldn’t try to time the market. Instead, it’s better to focus on how even a small change impacts your future mortgage payment.

Home Seekers • RE News •

January 31, 2025

INFOGRAPHIC: How Mortgage Rates Affect Your Monthly Payment

Home Seekers •

January 31, 2025

BLOG: What To Save For When Buying A Home

What To Save for When Buying a Home

Knowing what to budget for when buying a home may feel intimidating — but it doesn’t have to be. By understanding the costs you may encounter upfront, you can take control of the process.

Here are just a few things experts say you should be thinking about as you plan ahead.

1. Down Payment

Saving for your down payment is likely top of mind. But how much do you really need? A common misconception is that you have to put down 20% of the purchase price. But that’s not necessarily the case. Unless it’s specified by your loan type or lender, you don’t have to. There are some home loan options that require as little as 3.5% or even 0% down. An article from The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available . . .”

A trusted lender will go over the various loan types with you, any down payment requirements on those, and down payment assistance programs you may qualify for. The more you know ahead of time, the easier the process will be. And the key to getting the information you need is working with a pro to see what’ll work best for your situation.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various parties involved in your transaction. Bankrate explains:

“Mortgage closing costs are the fees associated with buying a home that you must pay on closing day. Closing costs typically range from 2 to 5 percent of the total loan amount, and they include fees for the appraisal, title insurance and origination and underwriting of the loan.”

When it comes to closing costs, a trusted lender can guide you through specifics and answer any questions you may have. They can also give you a better idea of how much you should be prepared to pay so you can cruise through your closing with confidence.

And as you plan ahead for closing day, be sure to budget for your real estate agent’s professional service fee too, in case the seller doesn’t cover it. But don’t worry, you’ll work with your agent ahead of time to agree on what this is, so you won’t be surprised at the finish line.

3. Earnest Money Deposit

And if you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). According to Realtor.com, an EMD is typically between 1% and 2% of the total home price and is money you pay as a show of good faith when you make an offer on a house.

But, it’s not an added expense. Instead, it works like a credit and goes toward some of your upfront costs. You’re simply using some of the money you’ve already saved for your purchase to show the seller you’re committed and serious about buying their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, this isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your local area. They’ll advise you on what moves you should make so you can make the best possible decisions throughout the buying process.

Bottom Line

The key to a successful homebuying savings strategy? Being informed about what you need to save for. Because, when you understand what to expect, you can plan ahead. With an expert agent and a trusted lender, you’ll have the information you need to move forward with confidence.

Home Sellers • RE News •

January 31, 2025

BLOG: Mortgage Forbearance

Mortgage Forbearance: A Helpful Option for Homeowners Facing Challenges

Let’s face it – life can throw some curveballs. Whether it’s a job loss, unexpected bills, or a natural disaster, financial struggles can happen to anyone. But here’s the good news. If you’re a homeowner feeling the squeeze, there’s a lifeline that many people don’t realize is still available: mortgage forbearance.

What Is Mortgage Forbearance?

As Bankrate explains:

“Mortgage forbearance is an option that allows borrowers to pause or lower their mortgage payments while dealing with a short-term crisis, such as a job loss, illness or other financial setback . . . When you can’t afford to pay your mortgage, forbearance gives you a chance to sort out your finances and get back on track.”

A common misconception is that forbearance was only accessible during the COVID-19 pandemic. While it did play a significant role in helping homeowners through that crisis, what many people don’t know is that forbearance is still a tool to support borrowers in times of need. Today, it remains a vital option to help homeowners in certain circumstances avoid delinquency and, ultimately, foreclosure.

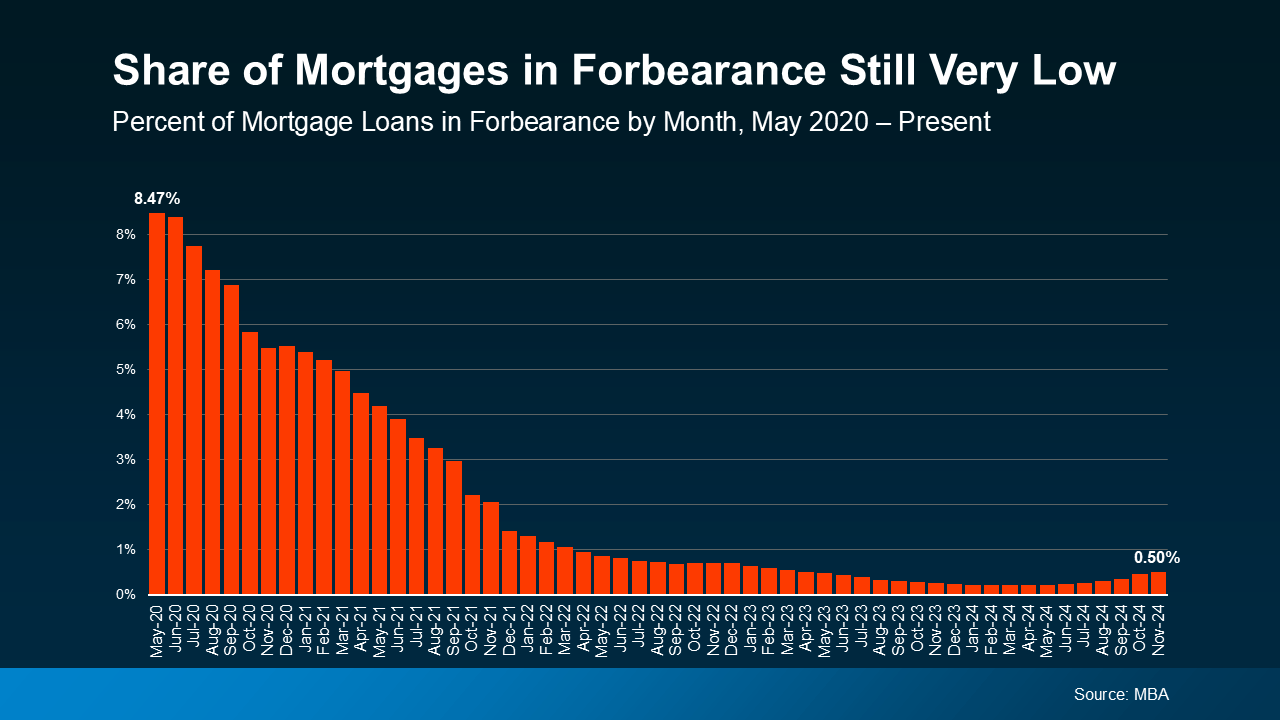

The Current State of Mortgage Forbearance

Forbearance continues to serve as a valuable safety net for homeowners facing temporary financial challenges. While the overall rate of forbearance has seen a slight increase recently, it’s important to understand what’s driving this change and how it fits into the broader picture.

According to Marina Walsh, VP of Industry Analysis at the Mortgage Bankers Association (MBA):

“The overall mortgage forbearance rate increased three basis points in November and has now risen for six consecutive months.”

This may seem concerning at first glance, but let’s break it down. The graph below, going all the way back to 2020, puts things into perspective:

While the share of mortgages in forbearance has significantly declined since its peak in mid-2020, there has been a slight but notable increase in recent months. This uptick is largely tied to the effects of two recent hurricanes — Helene and Milton.

While the share of mortgages in forbearance has significantly declined since its peak in mid-2020, there has been a slight but notable increase in recent months. This uptick is largely tied to the effects of two recent hurricanes — Helene and Milton.

Natural disasters like these often create temporary financial hardships for homeowners, making forbearance a crucial safety net during recovery. In fact, 46% of borrowers in forbearance today cite natural disasters as the reason for their financial struggles.

Even with the most recent uptick, the share of mortgages in forbearance is nowhere near pandemic levels, and, thankfully, reflects a very small portion of homeowners overall.

Why Forbearance Matters

Forbearance can help borrowers avoid the spiral of missed payments and foreclosure. It provides breathing room to address challenges and plan next steps. And while most homeowners today are not in a position to need forbearance, thanks to strong equity and foundations of the current housing market, it is an option for the few who do need it.

If you or a homeowner you know is facing financial difficulties, the first step is to contact your mortgage lender. They can walk you through the forbearance process and help you understand your options. Keep in mind that forbearance is not automatic — you need to apply and discuss the terms with your lender.

Bottom Line

In tough times, knowing your options can bring peace of mind. Forbearance isn’t just a financial tool — it’s a lifeline. And while the recent increase in forbearance rates might make headlines that give you pause, the truth is this option is working exactly as it should: helping those who need it most get through difficult moments without losing their homes.